(Spoiler: a small rise in sales doesn’t mean the market is healthy — it’s a patchy, fragile bounce with warning signs.)

Over the last few months headlines have been celebrating a “bounce” in Canadian home sales. August 2025 produced the strongest August sales pace in several years — sales were up versus last year and have climbed month-to-month since March. That sounds hopeful on the surface, but when you peel back the numbers the story looks a lot less rosy. The rise in transactions is happening alongside surging inventory, falling benchmark prices, collapsing housing starts, and economic weakness that’s forcing central bankers to consider rate cuts. Put together, those datapoints point to a market that’s settling into weakness, not recovering healthily.

The headline: sales are up — but only a little

The Canadian Real Estate Association reported roughly 40,257 sales in August 2025, about 1.9% higher than August 2024 and the fifth straight monthly increase since March. That’s the fact that’s getting repeated everywhere.

But important context: that increase is small in absolute terms and comes from a very depressed baseline after a deep cooling in 2024. In other words, we’re seeing a modest uptick off a low point — not a roaring recovery.

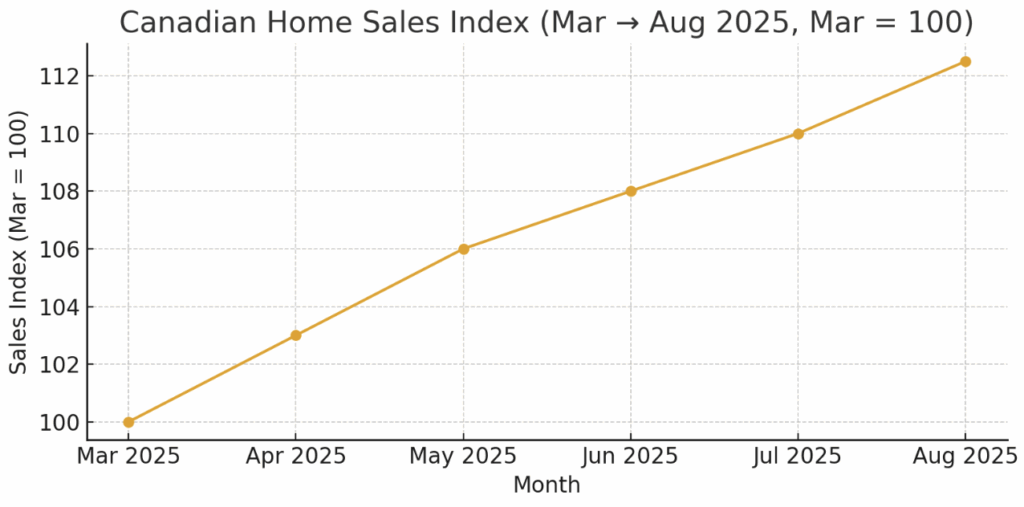

(See Chart 1: a normalized sales index showing March → August 2025 rising ~12.5% cumulatively. The index makes the increase visible, but it’s a gentle slope, not an exponential rebound.)

Inventory is growing — fast

If transactions were rising because demand had suddenly returned in force, we’d expect rising sales to push inventory down. The opposite is happening. Active listings across Canadian MLS systems were ~195,453 at the end of August 2025, up 8.8% year-over-year. That means more homes are available now than a year ago — which weakens seller pricing power and makes the market more buyer-friendly, but it also signals that supply is outpacing real, sustainable demand.

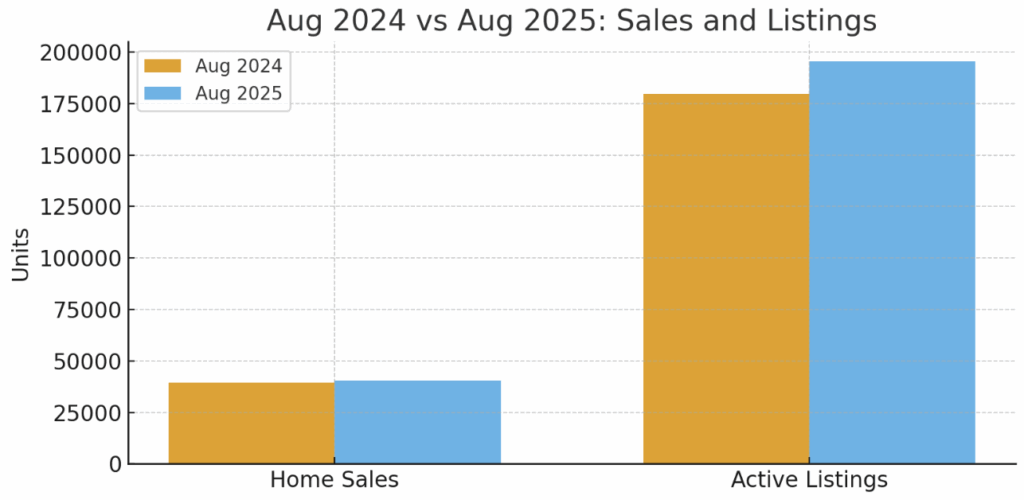

Chart 2 shows the contrast: August 2024 vs August 2025 for both sales and active listings. Sales ticked up slightly; listings rose materially. That imbalance is exactly why a small rise in sales doesn’t equal market strength.

Prices are not holding — benchmark price trend is down year-over-year

Even with the small sales bump, the MLS® Home Price Index (national composite) is still lower than a year ago. The benchmark fell about 3.4% year-over-year in recent figures, and month-to-month the index has been largely flat or slightly down after the big fall in late 2024. That tells you prices aren’t recovering in any meaningful way. Sellers are competing harder now, and buyers who thought a “sales bump” would push prices back up are likely to be disappointed.

New construction is collapsing — a future supply oddity

Housing starts aren’t supporting a healthy market either: the Canadian Mortgage and Housing Corporation (CMHC) reported a sharp 16% drop in housing starts in August 2025 compared with July — a surprisingly large monthly decline that shows builders are pausing or delaying projects. A fall in starts sounds like it would ease future supply — but in the short term it signals builder caution and economic unease (builders stop when financing is tight or demand looks shaky). It’s not an immediate fix for inventory imbalances.

Macro weakness and an incoming rate cut change the dynamic

Macro indicators are shifting in a way that undercuts a classic “boom.” Inflation has cooled enough that markets and many economists expect the Bank of Canada to cut rates (polls and market pricing show high odds of a 25 bps cut in mid-September 2025). Lower rates would normally help homebuying activity — but they’re also a signal that the economy is weakening, which suppresses wage growth and buyer confidence. The upshot: buyers may get cheaper credit, but some will still stay on the sidelines because incomes and job prospects are softer. That combination favors opportunistic buyers (investors, cash buyers) rather than broad-based recovery.

Why the “rise in sales” can be misleading

- It’s a rate effect off a low base. A few months of rising transactions after a slump doesn’t necessarily mean fundamentals improved — it can mean opportunistic buying, bargain hunting, or seasonal effects.

- Listings are rising faster than sales. When new listings outpace transactions, months-of-inventory rises and negotiating leverage shifts toward buyers. That dampens price growth, which is exactly what we’re seeing.

- Prices are still below last year. Buyers may be tempted to think a sales uptick means prices will shoot up; instead prices have been flat to down and remain below prior peaks.

- Builders look nervous. A large drop in housing starts is not a vote of confidence from the construction sector; it’s a sign the private sector isn’t convinced about future demand.

Put simply: more transactions in August were not enough to absorb the increase in inventory or reverse the price declines. The market has shifted from “seller’s market” to something more fragile and regionally uneven.

Regional nuance — not all markets behave the same

It’s worth underscoring that these national figures hide a lot of regional variation. Some markets (Vancouver, parts of Southern Ontario) have shown stronger month-to-month rebounds; others are still bleeding transactions and prices. In Ontario, for example, active listings hit unusually high levels in mid-2025 (inventory metrics in many Ontario markets remain elevated relative to long-run averages). That means local market strategy matters: a buyer in Toronto may see very different dynamics than a buyer in a smaller Ontario city.

What buyers should actually do (practical, defensive playbook)

If you’re a homebuyer watching the headlines and wondering whether now is the time to pounce, here’s a realistic checklist based on how the facts line up:

- Don’t assume prices will rebound quickly. The national benchmark is down year-over-year — plan for sideways-to-downward pressure in many markets.

- Use increased inventory to negotiate. More listings mean sellers may accept concessions (closing dates, repairs, price). Shop around rather than jumping the first time a house appears.

- Lock in mortgages only after you’re comfortable with job prospects. Rate cuts may make mortgages cheaper later, but if the economic picture weakens your employment risk increases — buy only if your finances are solid.

- Consider conditional offers and inspections seriously. Sellers who need to move may accept conditional offers; use inspection leverage to lower price or require fixes.

- Watch local supply metrics. National headlines hide local differences — track months-of-inventory and new listings in your specific city or neighbourhood.

What sellers should expect

If you’re trying to sell — be prepared for longer marketing times and tougher negotiations in many regions. The combination of rising listings and falling benchmark prices means you’re likely competing with more options for buyers. Pricing strategically (and realistically) will beat waiting for a market “snapback” that may not come.

Quick recap (the data points that matter)

- Sales: Small month-to-month gains; August 2025 sales ~40,257 (best August since 2021 but still modest).

- Listings: Active listings ≈ 195,453 (up ~8.8% YoY), showing higher supply.

- Prices: National MLS® HPI still down ~3.4% YoY — no broad recovery in prices yet.

- Starts: CMHC showed a 16% drop in housing starts in August — builders are pulling back.

- Rates: Markets expect the Bank of Canada to cut rates soon — a sign of economic weakness, not unequivocal relief.

Bottom line

Yes — home sales have risen modestly since spring. But that single metric doesn’t change the larger picture: inventories are higher, benchmark prices are down year-over-year, new construction is slowing, and central bankers are pivoting because the economy is weakening. The result is a fragile, uneven housing landscape where bargains exist, but recovery is neither broad nor certain.

If you’re a buyer, that likely means opportunity — but it also means caution. If you’re a seller, plan for a longer sell process and price competitively. SLG Home Buyer can help navigate this kind of market.